What Obamacare Fixed, and How Republicans constantly try to spin it as bad

Introduction

For decades, Americans wanted a health care system that worked the way people assumed it should. Stable. Fair. Affordable. Predictable. But the old system made that impossible. The Affordable Care Act (ACA), usually called Obamacare, was the first major attempt to fix those failures. It didn’t solve every problem, but it targeted the most brutal ones. And from the moment it was proposed, Republicans fought it with everything they had. Because it was not their idea. They to this very day have no ideas or counter proposals for healthcare other than making people pay 3x premiums.

1. What Americans Wanted Before Obamacare

A. Coverage that didn’t disappear

People wanted insurance that stayed with them even through job changes, illness, or major life events.

B. Protection for pre-existing conditions

Parents wanted kids with asthma, diabetes, or birth defects to be protected for life. Adults didn’t want to fear bankruptcy because they once had cancer.

C. Affordable premiums and deductibles

Ordinary people wanted plans they could pay for without giving up half their paycheck.

D. A working individual market

A system where freelancers, gig workers, and small-business owners could buy coverage without being punished for being human.

E. Relief from abusive insurance practices

Americans wanted an end to rescissions, surprise denials, lifetime caps, fine-print exclusions, and plans that fell apart the moment they were needed.

F. A basic sense of fairness

People didn’t expect miracles. They expected a system where being sick didn’t ruin your life.

2. Why Those Goals Were Impossible Before the ACA

A. Insurance companies made money by avoiding sick people

The business model rewarded denying care, excluding conditions, dumping patients, and cherry-picking the healthiest customers.

B. There were no national rules

Your protections depended entirely on your state. Most states had weak regulations. Some had almost nothing.

C. Coverage was wildly inconsistent

Two people with the same diagnosis could face wildly different outcomes depending on their zip code, employer, or insurer.

D. The individual market was structurally broken

Healthy people avoided it. Sick people had no choice. Prices spiraled. Risk pools collapsed. The system simply couldn’t balance itself.

E. Medicaid left millions behind

Most low-income adults didn’t qualify, especially in the South and Midwest. Millions worked full-time and still couldn’t get insurance.

F. Plans looked cheap but covered nothing

“Junk plans” had low premiums and massive loopholes. Many families didn’t realize they were one illness away from disaster.

Bottom line

The system worked for insurers and employers. It did not work for ordinary Americans.

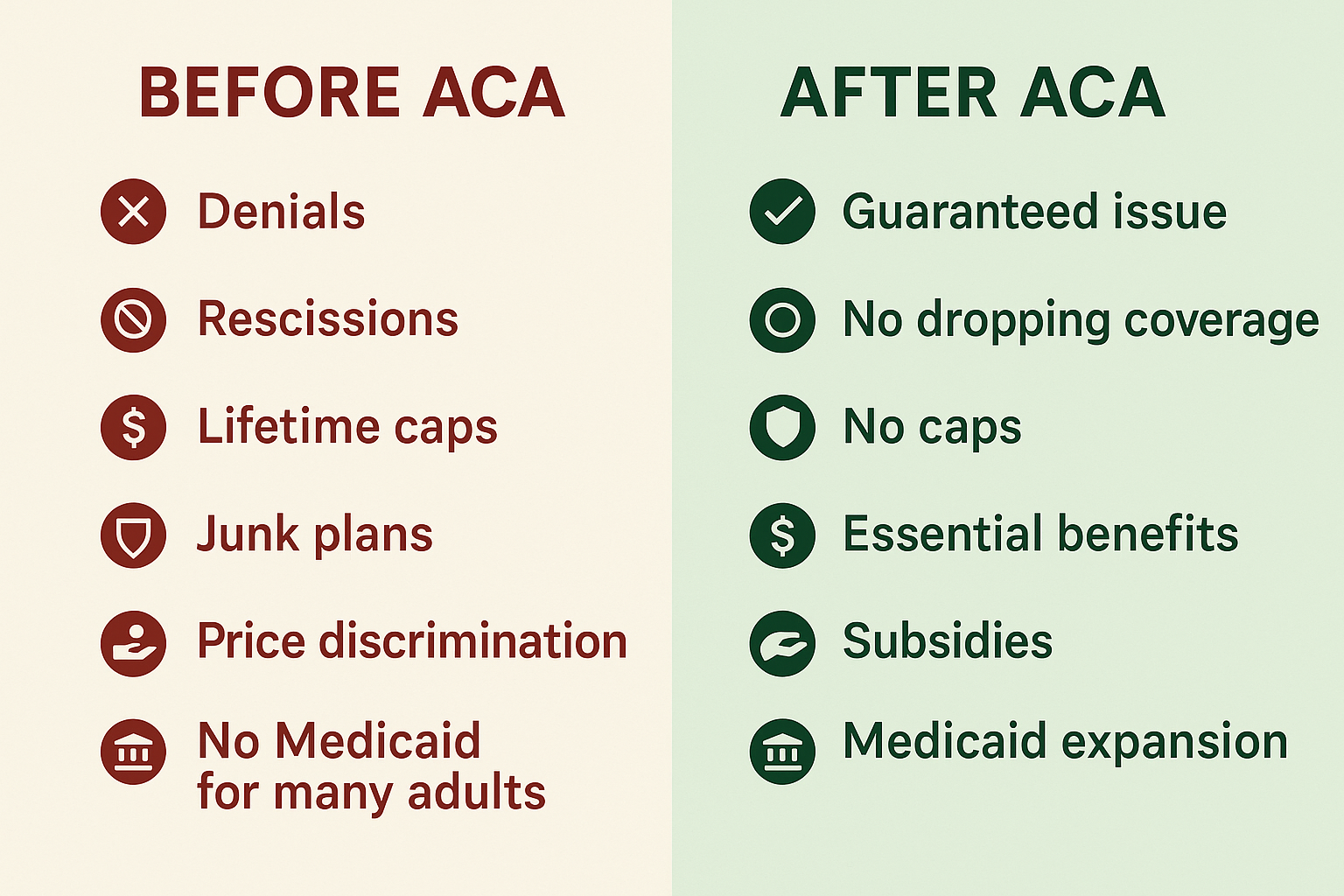

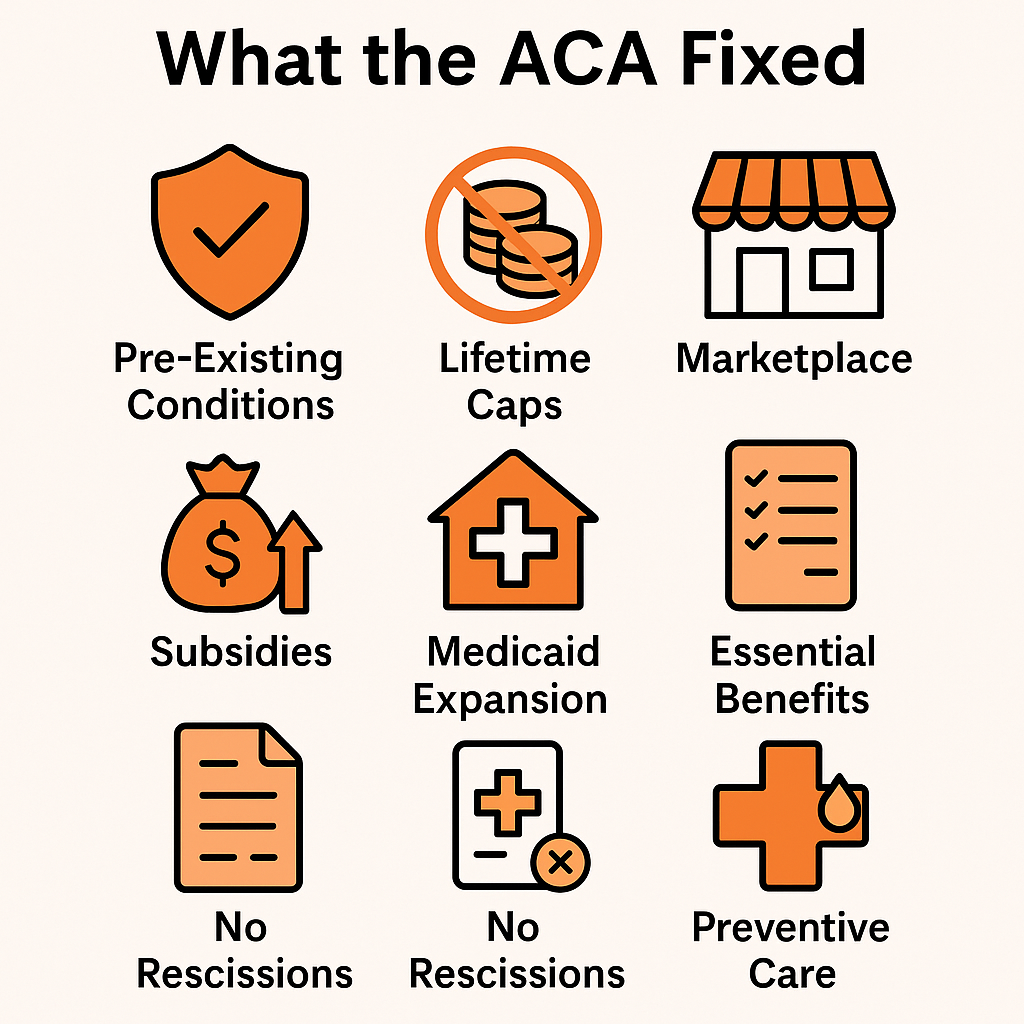

3. What Obamacare Actually Changed

A. Guaranteed coverage for pre-existing conditions

No more denials. No more price hikes because you were sick. This was the heart of the law.

B. Real standards for real insurance

Plans had to cover essential services: doctor visits, ER care, prescriptions, maternity care, mental health, chronic care, and preventive services.

C. Financial help to make insurance affordable

Premium subsidies and out-of-pocket caps opened the door for middle-class families. Medicaid expansion covered millions who previously had nothing.

D. Functional insurance marketplaces

Instead of chaos, the marketplaces standardized plans, created competition, and stabilized premiums across regions.

E. Removal of predatory practices

No lifetime limits. No rescission. No hidden exclusions. No more “fine print wins, patient loses.”

F. A national baseline of fairness

For the first time, your zip code didn’t determine your rights.

4. Why Republicans Fought It

A. Ideological opposition

The ACA expanded federal authority, set rules for private insurance, and strengthened public programs. Many Republicans reject that model entirely.

B. Political strategy

GOP leaders openly said their goal was to block Obama on everything. Killing Obamacare became the core of that strategy.

C. Fear of a new, popular entitlement

If the ACA succeeded, it would become politically untouchable. That terrified Republicans. Eliminating protections for pre-existing conditions would be political suicide.

D. Pressure from donors and industry allies

Some insurers and conservative think tanks hated the new rules restricting discrimination and limiting profit margins.

E. Weaponized misinformation

“Death panels,” “government takeover,” “you’ll lose your doctor.” These claims stirred fear but didn’t reflect the actual law.

F. Repeal became a loyalty test

For nearly a decade, every Republican candidate had to promise to repeal the ACA. It became an identity issue, not a policy debate.

Despite dozens of repeal attempts — and one near-failure in 2017 — the ACA survived and became extremely popular.

5. What the ACA Did for Regular People

A. Tens of millions gained coverage

This was the largest health insurance expansion since Medicare.

B. Protections became universal

No insurer in America can deny, drop, or price-gouge someone because they have a pre-existing condition.

C. Coverage became more predictable

People could finally switch jobs, start a business, or get sick without losing insurance.

D. Financial security increased

Families were no longer wiped out by hidden exclusions or lifetime caps.

E. The system became more transparent

Standardized plan tiers and essential benefits made it easier to compare and choose coverage.

What’s Happening Now & How the ACA Will Change

What has been passed

- The One Big Beautiful Bill Act (OBBBA) includes sweeping tax, spending and health-care cuts. Wikipedia+2KFF+2

- Among its health-care related measures, the bill enacts major changes to federal spending on Medicaid and majorly reduces criteria for ACA marketplace support. Bloomberg School of Public Health+3AP News+3The Washington Post+3

- A continuing resolution signed November 2025 did not extend enhanced premium tax credits for ACA plans — putting millions at risk of premium hikes. CMADocs+1

Key changes and impacts for the ACA

- Subsidies expire or shrink: Enhanced ACA premium tax credits (expanded during the pandemic) are slated to end at end of 2025. Without them, premiums for 2026 are projected to rise sharply. Brookings+1

- Eligibility and requirements tighten: New rules shorten open enrollment periods, impose enrollment fees, and change eligibility documentation, raising barriers for some ACA marketplace enrollees. Like they are trying to find ways to cut more people out of support with intentionally difficult requirements. Reuters

- Medicaid cuts and influence on ACA expansion: The bill accelerates work and reporting requirements for Medicaid, and reduces incentives for states to expand Medicaid under the ACA. This threatens the “coverage ladder” the ACA built. Politico+1

- Overall coverage loss expected: Independent estimates suggest that millions of Americans could lose health insurance because of the combined effect of subsidy expiration, eligibility tight-downs and Medicaid cuts. The Washington Post

Why this matters

- Many of the protections and affordability mechanisms of the ACA depend on robust subsidies and state Medicaid expansion. When those are scaled back, the “fixes” the ACA provided become more fragile.

- Rising premiums and lower eligibility mean the ACA’s gains (expanded coverage, protection against pre-existing condition discrimination, more affordable plans) may unwind for many Americans.

- Politically, this marks a major shift: instead of incremental tweaks, this is a broad rollback of the structural supports that undergirded the ACA since 2010.

What to watch

- Whether Congress extends the enhanced premium tax credits or allows them to expire. Their extension would blunt some of the damage.

- How states respond: will more states reject Medicaid expansion or accept the tighter rules, and how will that affect coverage rates?

- Litigation: Several states are suing over proposed ACA marketplace rule changes. Outcomes could delay or alter the implementation of disruptive changes. Reuters

- Rate changes for 2026: Because subsidies are shrinking, insurers are already signaling major premium increases in many states. Brookings+1

Conclusion

The ACA was built to correct the deep dysfunctions of the U.S. health-insurance market. It expanded coverage, made plans usable, curbed predatory practices. But now the 2025 legislative changes represent a pivot away from reinforcement and toward rollback. For regular people, the protections they’ve come to rely on could be weakened or unaffordable — unless stabilizing action (subsidy extension, state responses, courts) intervenes.

Forecast Box: What 2026–2030 Could Look Like for the ACA

Best-Case Scenario (Stabilized but Weakened ACA)

Assumes:

• Congress restores enhanced subsidies

• States adapt flexibly to Medicaid rule changes

• Courts block the most disruptive marketplace restrictions

Estimated Outcomes:

- Coverage losses: ~5–8 million people

- Average premiums (ACA marketplaces): +18 to +28 percent

- Medicaid enrollment: modest decline, ~2–3 million people

- Marketplace stability: moderate; some insurers exit high-risk states

- Pre-existing condition protections: stay intact legally, but less usable due to higher cost

- Net effect: The ACA survives with visible damage but remains functional for most people.

Middle-Case Scenario (Significant Erosion)

Assumes:

• Subsidies expire fully

• Medicaid work/reporting requirements fully enforced

• Marketplace fees and enrollment barriers go into effect

• Limited court intervention

Estimated Outcomes:

- Coverage losses: ~12–17 million people

(This matches independent forecasts already reported by major media.) - Average premiums: +35 to +60 percent by 2028

- Medicaid enrollment: down ~5–8 million

- Marketplace stability: growing insurer withdrawals in rural states; fewer plan choices

- Pre-existing condition protections: legally intact but functionally weakened due to cost barriers

- Net effect: The ACA is still “alive” on paper, but affordability and access shrink dramatically.

Worst-Case Scenario (Structural Breakdown of ACA Coverage)

Assumes:

• Subsidies end with no replacement

• Deep Medicaid reductions

• Marketplace changes survive court challenges

• Additional administrative rules tighten eligibility further

• Insurer exits accelerate

Estimated Outcomes:

- Coverage losses: ~22–28 million people by 2030

- Average premiums: +70 to +120 percent

(Driven by healthier people exiting the market entirely.) - Medicaid enrollment: down ~10–14 million

- Marketplace stability: several states left with 0–1 carriers

- Pre-existing condition protections: technically exist, practically meaningless due to unaffordable premiums

- Net effect: The ACA’s core structure collapses. Coverage reverts toward the pre-2010 system:

• high uninsured rates

• unstable individual markets

• growing medical debt

• broad return of state-by-state inequality.

But don't worry!

Millionaires and Billionaires will pay less taxes than ever!. The wealthiest 400 families paid an average federal individual tax rate of just 8.2% when their wealth increases were counted as income. By comparison, the average American taxpayer in the same period had an average effective tax rate of about 30%. Top labor earners pay an effective tax rate of around 45%. In 1975, the top marginal U.S. federal income tax rate was 70%, but a special provision limited the effective tax rate on earned income to 50%. And there were not so many loopholes on income wealth back then also.

When people say our country is in debt and can't pay and is going to go bankrupt ... I call bullshit. We are just subsidizing the wealthy. Capitalism is not quite working as intended.

Comments ()